According to new revenue estimates by PokerScout, the highest-grossing network in regulated US online poker is either BetMGM or WSOP, depending on the time of year. For most of the past year, it has been BetMGM at the top of the heap, but added traffic from tie-ins with the live World Series of Poker propels WSOP ahead during the summer months.

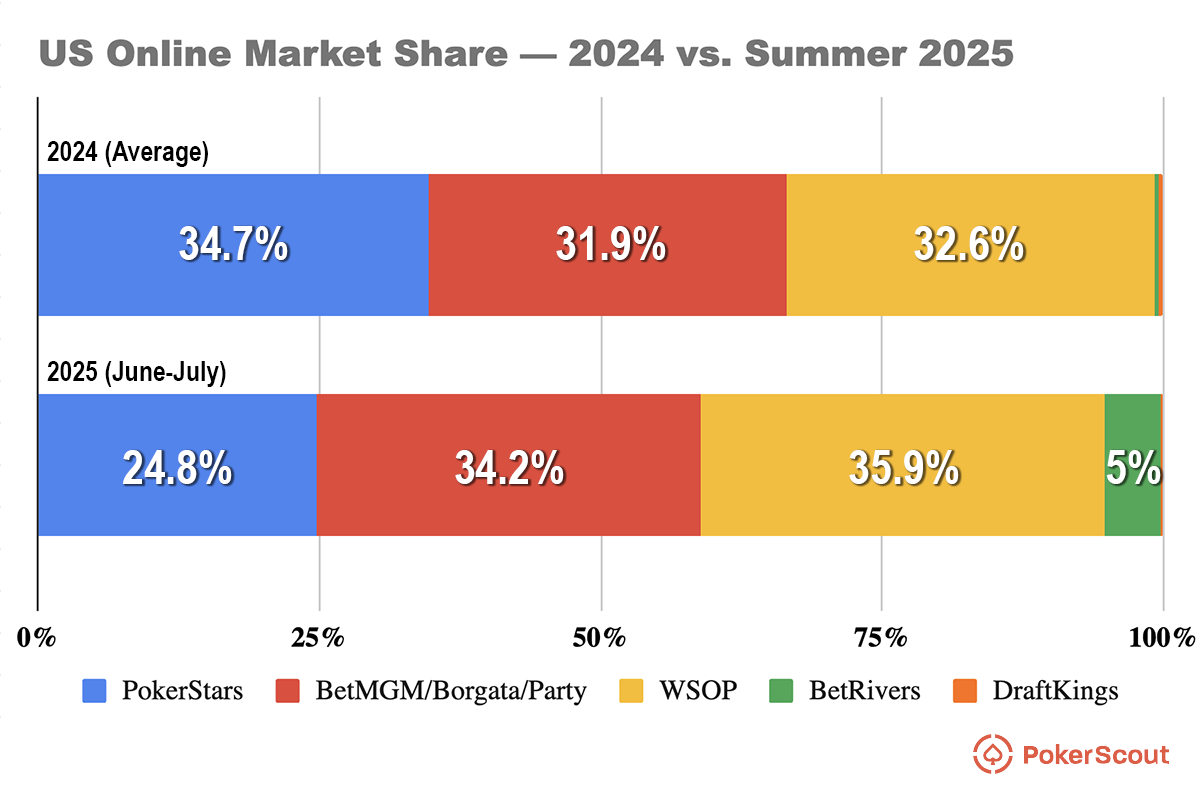

The two new leaders have about 35% of the market each, give or take a few percent each month. It’s not a big market compared to online casino gaming, but it will be producing an estimated $10 million per month by early next year. The entry of Pennsylvania into the Multi-State Internet Gaming Agreement appears to be the main factor driving recent growth.

While the battle rages on up top, BetRivers is a small but rapidly emerging competitor now that it has gone multi-state. It still only has 5% of the market, but that figure has been rising steadily.

On the other hand, PokerStars is on a negative trajectory, down 10 percentage points in market share since 2024, despite having been the comfortable market leader for many years. The fact that it’s the only network to have left Pennsylvanians cut off from other states is part of the reason. However, the downturn began well before June, when Pennsylvania was added to competitors’ networks.

Overall, the market for regulated online poker in the US looks very different now than it did one year ago, which is surprising given that it had been largely static from 2021 to 2024. A change in market share lead is only part of that. There are also new states online and new players in the market, and total revenue has grown by about 15% after years of stagnation.

Keep Reading

Last year, PokerStars held 35% of the total market, a position similar to that now enjoyed by BetMGM and WSOP. Those latter brands accounted for about 32% each, while DraftKings and BetRivers, which entered the scene late in the year, generated only about 1% of the year’s revenue between them.

PokerStars’s dominance was already starting to show signs of waning by that point. In January 2024, its market share was 39%. By August, it was in a three-way tie with BetMGM and WSOP.

Then, BetRivers launched in Pennsylvania and began pulling market share mostly from PokerStars, while BetMGM and WSOP continued apace. By the end of the year, it was already BetMGM out in front.

The networking of Pennsylvania didn’t come until April this year. When that happened, however, it produced a considerable acceleration of the trend. PokerStars’ estimated market share cratered by seven percentage points in two months, from 32% in March to 25% in June.

BetRivers has emerged from nowhere to claim a respectable 5% market share and continues to grow month over month. It’s too early to tell where it will stop. Conversely, DraftKings only dipped its toe into poker with Electric Poker, an ultra-fast, three-player format integrated into DraftKings Casino, which appears to have been something of a flop with players.

Local Focus Seems to Be the Key

PokerStars has cited “international priorities” when explaining its decision to postpone making the effort to integrate Pennsylvania. Conversely, BetMGM and BetRivers have focused their poker efforts entirely on the U.S., as did WSOP until its recent acquisition by GGPoker.

That difference in focus and prioritization may have been the reason for PokerStars’ earlier decline as well. Even a cursory examination of the brands’ feedback channels on the US Poker Community Discord server reveals a noticeable difference in tone, with players seeming grateful to BetMGM’s responsiveness to feedback, while displaying a cynical attitude toward PokerStars.

The tone in BetRivers’ channel is similarly upbeat, though it’s obvious that the new operator is still a work in progress in some regards. As for WSOP, the channel name itself tells a story: #no-wsop-reps-exist-talk-to-a-wall-here.

So, BetMGM and BetRivers appear to be focused on their players, WSOP is relying on the popularity of the live series to carry the site, and PokerStars’ owner Flutter may be losing interest in brands other than FanDuel for the U.S. market.

BetMGM’s market share peaked in May at 40%, just before the live World Series of Poker got underway. The following month, that dropped to 33% while WSOP took the lead with 38%. Now that the series is over, we’re seeing a shift back toward BetMGM dominance that should continue through the fall.

Is Michigan Low-Key the Biggest U.S. Online Poker Market?

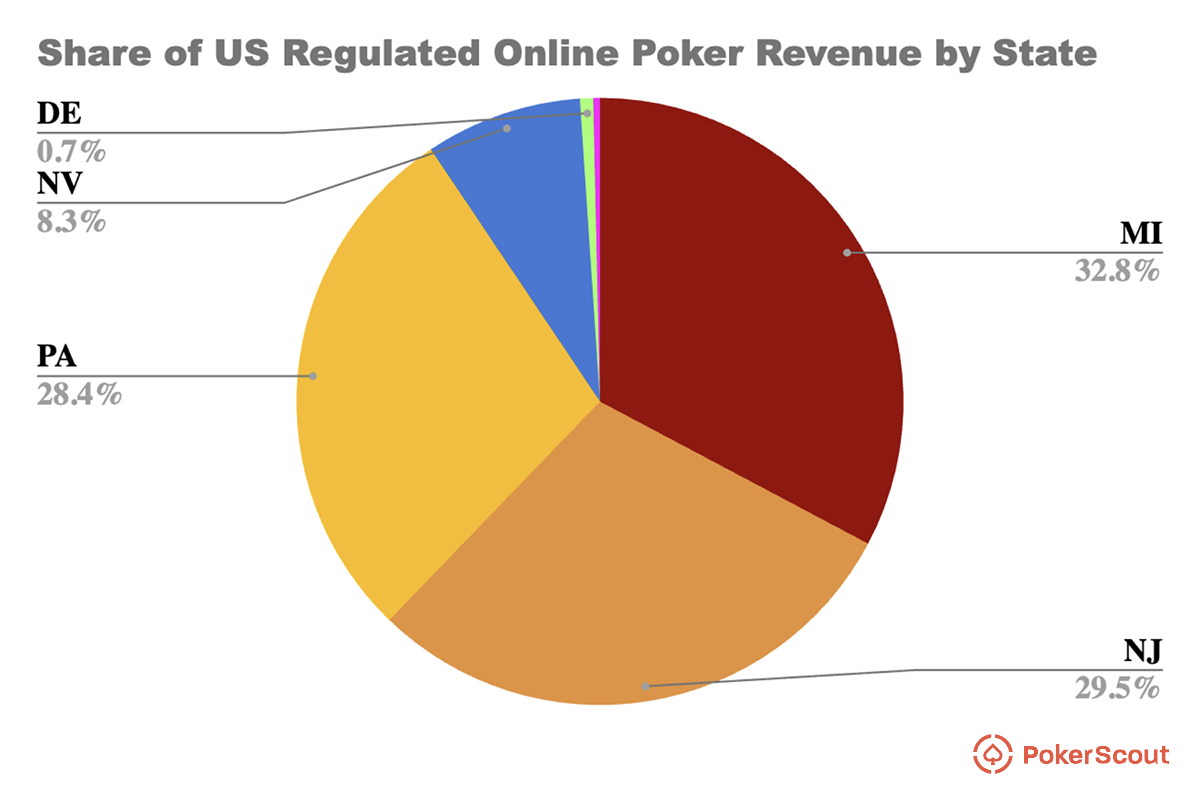

Calculating the U.S. online poker market is difficult and involves a fair bit of estimation and guesswork. Each state reports iGaming revenue differently, and the only one supplying exact poker numbers for each individual brand is New Jersey. We can also include Delaware, by virtue of the fact that it’s a BetRivers monopoly.

You won’t hear much talk about Michigan online poker revenue because that state’s regulator lumps it in with the online casinos. The best we can do is to look at how BetMGM, PokerStars, BetRivers, and Caesars (WSOP) are doing overall, and guess that poker amounts for a similar percentage of that revenue as it does in other states. And that percentage is very small, around 2%.

Under that assumption, Michigan turns out to be the most important U.S. market—ahead even of Pennsylvania, which has 3 million more residents. By PokerScout’s estimate, Michigan accounts for about 33% of the US market, while Pennsylvania and New Jersey account for less than 30% apiece.

Although that’s something of a guess, there are reasons to believe it’s accurate. Michigan has a larger population than New Jersey. Having launched in 2021, it also brought players the most up-to-date software, whereas WSOP players in New Jersey were stuck on an older, buggy client for several years. While it’s a smaller state than Pennsylvania, its iGaming rollout went much more smoothly, and it was much quicker to join MSIGA and allow multi-state poker.

What we can say for certain is that New Jersey and Pennsylvania are very similarly-sized markets, despite Pennsylvania’s player base being roughly 40% larger. That’s surely the impact of a rough, staggered iGaming rollout in Pennsylvania, and long delays in getting it networked with other states. We can expect Pennsylvania to drive growth now that the situation has changed.